High Returns, High Risks: Construction Lending Challenges Private Lenders

Lending on construction projects can be an exciting growth area for private and non-bank lenders. With more entrants into the market, competition is high—and so is the opportunity for outsized returns. However, construction lending comes with unique and often underestimated risks that differ greatly from traditional real estate or business loans.

As the president of a company focused on construction risk management, I’ve seen firsthand how challenging it can be for lenders—especially private lenders—to navigate the complexities of construction due diligence and project oversight. Non-bank lenders are often experts at number crunching and spotting deals that “pencil out” from an investment standpoint. However, the reality is that successful project completion depends on far more than financial modeling.

The Hidden Risks of Construction Lending

Traditional lenders have large infrastructure behind them: risk management staff, engineers, and construction loan administrators. Many private lenders, however, operate with lean teams. While this agility is a business advantage, it comes with unique challenges:

- Underwriting Contractor Qualifications: Many lenders focus on pro formas and appraisals but may not rigorously assess if the general contractor has the right experience, resources, and financial stability to deliver the project.

- Evaluating Plans, Specs, and Budgets: Even if the numbers look good, do the plans actually support the desired product? Is the budget realistic, and are all necessary line items included?

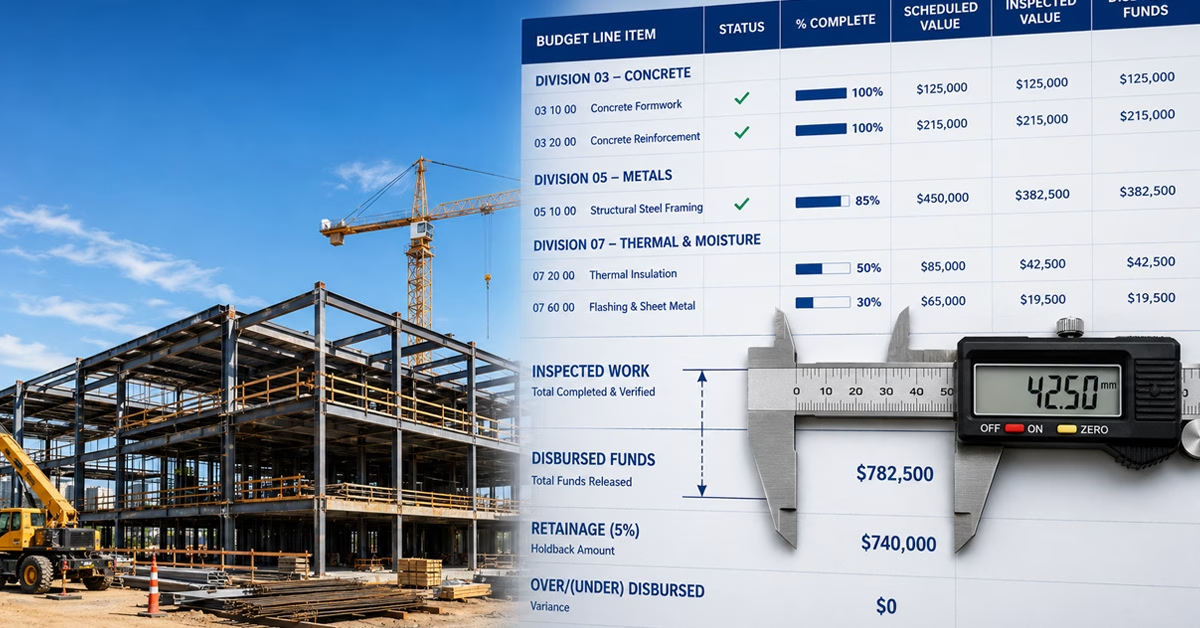

- Draw Management and Documentation: Progress draws must be carefully managed to reduce risk. Without the right protocols, lenders may inadvertently release funds before sufficient work is completed or before proper documentation (like lien waivers and change order logs) is in place.

- Third-Party Inspections: Lenders may rely on third-party inspectors to protect their position — but not all inspectors are created equal. It’s not just about getting a report; interpreting it accurately is critical.

- Managing Risks Post-Closing: Construction projects evolve. Unanticipated delays, cost overruns, or issues with approvals can arise, and lenders need protocols to identify potential red flags before they become crises.

Why a Proactive, Expert Approach Matters

Too often, private lenders rely on “instinct” or basic guidelines that may work for stabilized assets but fall short in construction scenarios. This can lead to costly mistakes. For example:

- Funds disbursed too early, before work is complete.

- Approving draw requests without confirming if changes have been made (and whether those changes were documented and budgeted correctly).

- Overlooking the importance of lien waivers and legal documentation, resulting in exposure to mechanic’s liens or contractor disputes.

- Failing to spot early signs of contractor stress, such as slow mobilization or inconsistent job site progress.

Best Practices for Private Lenders

If this sounds daunting—don’t worry. You don’t have to become a construction expert overnight. Here are some practical steps:

- Engage Specialized Risk Management: Partner with professionals who understand construction, from plans and specs to job cost ledgers and inspection protocols. They can translate “builder speak” into actionable risk assessments.

- Develop a Construction Due Diligence Checklist: Ensure your underwriting process includes contractor background checks, detailed budget reviews, and plan/specs verification—not just a financial pro forma.

- Set Up Robust Draw and Disbursement Systems: Standardize processes for submission, review, approval, and documentation of draws. Require independent inspections and always obtain lien waivers.

- Continuous Monitoring: Maintain regular project communication, random site visits, and keep documentation up to date. Don’t just “set it and forget it.”

- Education & Process Improvement: Even a little training can go a long way. Make construction risk management a core competency of your lending business.

Conclusion: We’re Here to Help

You know how to spot a great deal; CFSI Loan Management knows how to protect your investment through every phase of construction. The right partnership means you can offer attractive construction loans while safeguarding your capital and your reputation. If you have questions or want to explore how we can help shore up your construction lending processes, let’s start that conversation.

Remember, in construction lending, successful projects don’t just pencil—they stand the test of time. Let’s build something great, together.