Key Strategies to Protect Capital and Prevent Fraud

As we enter 2026, construction lending is undergoing a profound shift. The market isn’t crashing—it’s tightening. Liquidity is more selective, margins are compressed, and borrowers face stretched resources amid lingering inflation and interest rate pressures. Lenders who thrive won’t be the most aggressive; they’ll be the most intelligent, prioritizing verified progress, strict draw discipline, and data-driven oversight.

This blog post summarizes the 2026 Construction Lending Risk Survival Guide, a practical resource drawn from nearly two decades of nationwide experience in residential, commercial, and multifamily projects. The full guide is available as a complimentary white paper download—perfect for lenders seeking operational strategies to safeguard capital.

The 2026 Construction Lending Landscape: Where Risks Are Rising

Today's exposures include:

- Mid-cycle project defaults

- Borrower liquidity burnout from rate resets and delayed financing

- Scope creep due to labor and material cost volatility

- Overloaded contractors juggling multiple jobs

- Outdated budgets that no longer match reality

Execution risk—not the loan itself—drives vulnerability. Traditional inspection-only approaches fall short when progress turns uncertain.

Effective mitigations for 2026 include:

- Volatile costs → Continuous budget-to-progress reconciliation

- Borrower strain → Early cash-flow warning systems

- Contractor overload → Performance scoring and experience verification

- Supply chain issues → Proof of material delivery and installation

- Sophisticated fraud → Independent third-party data validation

Lenders who enforce slow, verified fund releases will outperform those rushing disbursements.

Modern Construction Fraud: Sophisticated, Organized, and Costly

Fraud in 2026 is polished and engineered, not amateur. Schemes feature aligned photos, invoices, and narratives designed to pass reviews. Common vectors:

- Progress inflation (the leading cause of losses)

- Duplicated invoices across parties

- Material substitution or downgrades

- Ghost labor billing

- Reused photos from other sites

- Collusion among borrower, contractor, and inspector

Fraud follows the classic triangle: pressure, opportunity, and rationalization. Document-only monitoring creates opportunity; adding field and behavioral checks closes it.

The Draw Failure Chain: How Losses Compound Quietly

Losses in construction lending begin early and compound quietly. It often starts with initial draws receiving light review, followed by scheduled releases to maintain momentum. Minor overruns are dismissed as normal, while the contractor’s cash flow weakens. Work slows, yet draws continue, leading to requests for accelerated funding “to stay on schedule.” Eventually, funding outpaces actual progress, shifting leverage to the contractor and requiring extra capital amid rising lien and litigation risks.

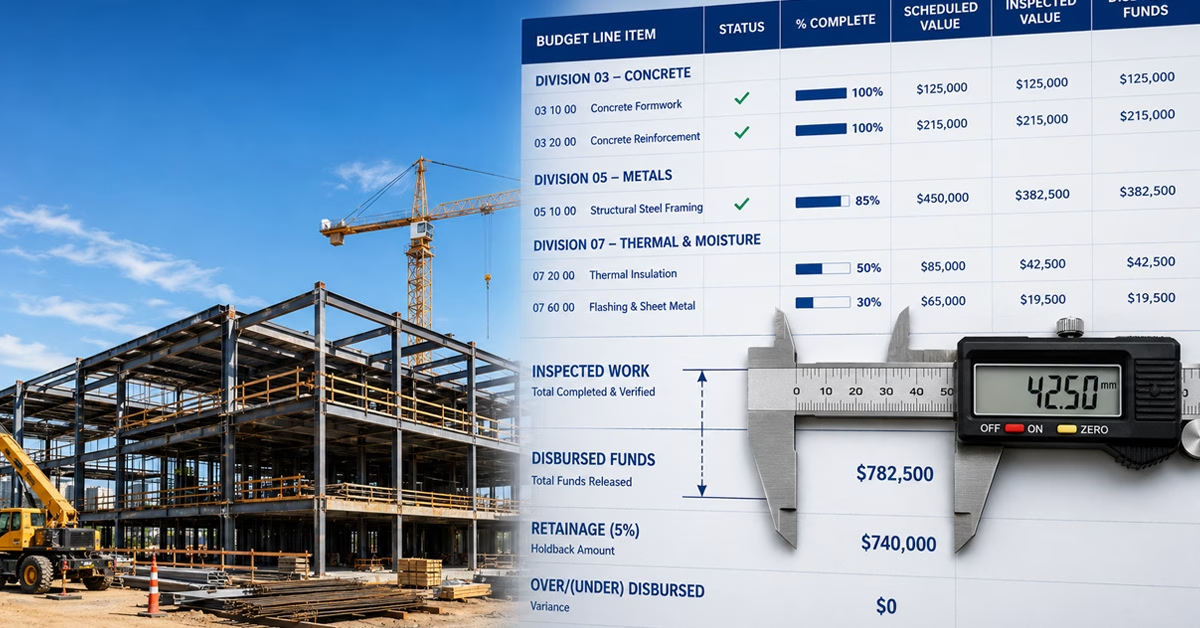

To prevent this, adhere to strict disbursement rules: Verify progress before releasing any funds. Never advance money ahead of confirmed physical completion. Confirm the correct site or parcel each time. Maintain material chain-of-custody from delivery to installation. Track change orders independently. Cross-check invoices against installed work. For complex projects, engage independent fund control. These measures turn draw management into reliable capital protection.

Why Traditional Inspections Alone Are Insufficient

Inspections show what's visible but miss hidden risks—staged sites, concealed quality issues, or wrong-lot errors. Geo-verification, timestamps, and independent controls are essential.

Case study: The Wrong Lot Disaster

A lender funded a subdivision based on appraisals and reports. The contractor built on the wrong parcel, supported by legitimate-appearing progress on a different lot. Draws flowed until plat updates revealed the error, leading to collusion discovery and major loss. Parcel verification and geo-locked reporting could have stopped it early.

Advanced Protection: The CFSi Framework and Nitro-AI Evolution

CFSi Loan Management delivers a proven six-stage model:

- Pre-close risk review

- Budget integrity analysis

- Controlled draw release

- Proof-based inspections (GPS, timestamps)

- Exception escalation

- Closeout lien protection

Their platform Nitro-AI elevates this with AI-driven capabilities:

- Geo-tagged evidence validation

- Predictive completion forecasting

- Contractor confidence scoring

- Anomaly detection

- Audit-ready reporting

This combination turns reactive lending into proactive, transparent control.

2026 Risk Survival Checklist

Check these to stay protected:

- No draw without verified progress

- Lot identity confirmed every inspection

- Contractors validated beyond references

- Independent change order tracking

- Continuous budget/timeline monitoring

- Geo-verified inspections

- Periodic contractor liquidity reviews

- Active fraud pattern monitoring

- Enforced closeout lien protocols

Discipline isn't restrictive—it's profitable. Download the full 2026 Construction Lending Risk Survival Guide white paper today and connect with the team at CFSi Loan Management to discuss reducing your exposure.