The commercial construction landscape in mid-2026 presents a sharp paradox for lenders. On one hand, top-line planning and starting metrics show strong momentum, propelled by a historical wave of technological infrastructure development. On the other hand, traditional sectors are softening, material costs are re-accelerating, and regulatory frameworks are introducing severe environmental traps at foreclosure. Meanwhile, private and non-bank lenders face highly sophisticated operational fraud schemes in their origination pipelines.

To protect capital and shield clients from catastrophic losses, lenders can no longer manage portfolios using cycle-past assumptions. This white paper analyzes the four critical risk vectors redefining construction lending in 2026 and outlines the modern safeguards required to preserve capital through project closeout.

1. The Macro Picture: The “Data Center Mirage” and Sector Divergence

At a glance, the construction market appears to be surging. Total construction starts jumped 13% in May 2026 to a seasonally adjusted annual rate of $1.16 trillion, driven by an 18% improvement in nonresidential building. Concurrently, the Dodge Momentum Index (DMI), which leads nonresidential construction spending by 12 to 18 months rose 5.9% to 275.7 in May, standing a striking 33.8% higher than May 2025.

However, digging beneath these headlining figures reveals an extreme sector concentration:

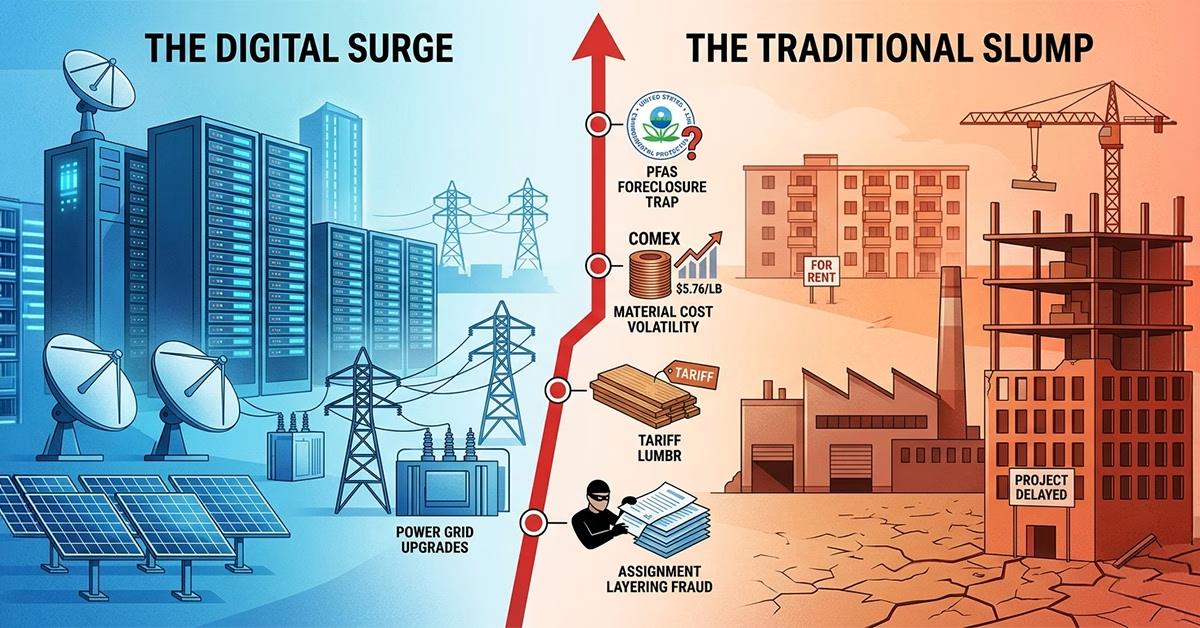

- The AI Infrastructure Boom: Combined office and data center starts jumped 214% year-to-date through April 2026, propelling overall nonresidential starts.

- The “Ex-Data Center” Reality: While year-over-year commercial planning grew 41.2% in May, that gain collapses to just 6.6% when data center projects are excluded. Over 85% of nonresidential year-to-date growth through April is concentrated in the data center ecosystem (offices/data centers, power generation, power transmission, and water/sewage).

- The Residential and Manufacturing Slump: Conversely, residential starts slumped 24% year-to-date (with single-family down 25% and apartments down 23%), while industrial manufacturing construction fell for its 14th consecutive month, declining 18% year-over-year.

| Sector Metric (Mid-2026 Trends) | Year-Over-Year / YTD Change | Market Implication |

|---|---|---|

| Combined Office & Data Center Starts | +214% YTD | Highly concentrated developer demand |

| Commercial Planning (with Data Centers) | +41.2% YoY | Distorts overall industry health indicators |

| Commercial Planning (excluding Data Centers) | +6.6% YoY | Reflects sluggish traditional commercial activity |

| Industrial Manufacturing Construction | -18.0% YoY | 14th consecutive monthly decline |

| Private Residential Starts | -24.0% YTD | Sharp downturn in housing supply velocity |

“In mid-2026, the construction index isn’t telling you that the whole market is booming, it’s telling you that the artificial intelligence gold rush is funding a massive digital footprint. Lenders must recognize this concentration risk.”

Financing non-data center commercial real estate requires rigorous, submarket-specific underwriting, as traditional asset classes are not experiencing the same rising tide as tech infrastructure.

2. The New Environmental Battlefield: PFAS and the Foreclosure Trap

Perhaps the most legally toxic hazard facing lenders in 2026 is the rapid evolution of federal environmental liability regarding per- and polyfluoroalkyl substances (PFAS), commonly known as “forever chemicals.”

In April 2024, the EPA finalized a rule designating two common PFAS subtypes (PFOA and PFOS) as hazardous substances under the Comprehensive Environmental Response, Compensation, and Liability Act (CERCLA). Despite ongoing litigation challenging the rule (Chamber of Commerce v. EPA), the Trump Administration confirmed in late 2025 that it intends to maintain and defend the designation. Furthermore, while the EPA proposed rules on May 18, 2026, to extend drinking water compliance timelines to 2031, the strict, retroactive joint and several liability under CERCLA remains fully in force.

This creates a massive loophole for lenders:

- The ASTM E1527-21 Loophole: The governing framework for Phase I Environmental Site Assessments (ESAs) is ASTM E1527-21. Under Section 13 of this standard, PFAS is classified as a “non-scope consideration”.

- The Foreclosure Risk: Because PFAS is a non-scope item, standard Phase I ESAs do not automatically evaluate it. If a lender forecloses on an asset with undetected PFAS contamination, they step into the chain of title and inherit absolute, retroactive liability for federal cleanup costs—even if they did not cause the contamination.

“Foreclosing on a property with undetected PFAS is the environmental equivalent of inheriting a blank check written to the EPA.”

To protect their collateral, lenders must explicitly instruct environmental consultants to add a dedicated, non-scope “PFAS screen” to all Phase I ESAs, particularly for properties near industrial zones, landfills, airports, or manufacturing hubs.

3. Material Cost Volatility and Tariff Pressures

Lenders must also contend with a re-acceleration of material cost inflation. Producer Price Index (PPI) data shows construction input prices climbed 6.6% year-over-year through April 2026, punctuated by a sharp 1.7% surge in April alone.

This volatility is driven by geopolitical conflicts and aggressive trade policies:

- Copper’s Digital Premium: COMEX copper is trading near $5.76/lb (+32% YoY), driven by AI data center demand, grid upgrades, and supply shocks at Freeport-McMoRan’s Grasberg mine in Indonesia.

- Metal and Softwood Tariffs: Section 232 tariffs on construction-critical metals remain at 50%. Softwood lumber imports face a punishing 10% tariff, keeping framing lumber around $872 per thousand board feet.

These rising input costs have outpaced contractor bids, threatening borrower margins.

“Uncapped material escalations are silent margin-killers. If your borrower’s budget doesn’t account for copper’s digital premium, you are under-collateralized before the first shovel hits the dirt.”

Lenders must enforce highly detailed budget contingency planning. Relying on historical cost baselines will lead to rapid under-capitalization of active projects.

4. Operational Hazards: Straw Buyers and Assignment Layering

In private and non-bank lending, operational fraud has evolved into a highly coordinated threat. As traditional lending standards have tightened, bad actors are deploying sophisticated schemes to bypass underwriting:

- Assignment Layering: Fraudsters utilize wholesale transactions to obscure their identities. By layering multiple contract assignments, they make it incredibly difficult for lenders to trace who originally entered the purchase agreement and who ultimately controls the borrowing entity.

- Straw Buyer Schemes: Disreputable operators who have previously defaulted or been blacklisted will enlist clean-name family members or newly formed shell entities to serve as the public-facing borrower. The true, high-risk operator remains behind the scenes, siphoning funds while shielding themselves from liability.

- The Scale of the Threat: This is not an isolated problem. CoreLogic’s Mortgage Application Fraud Risk Index recently highlighted that fraud applications for multiunit homes have spiked to a 3.5% fraud rate (one in 27 applications).

“Strict draw discipline and independent site verification aren’t hurdles to a project; they are the shields that protect your capital from empty promises.”

To combat these schemes, lenders must implement exhaustive KYC (Know Your Customer) due diligence that looks beyond newly formed LLCs. Furthermore, funds control must be governed by independent, third-party due diligence partners who conduct regular, geo-verified site inspections.

5. The Survival Playbook: Protecting Your Portfolio

To mitigate these compounding risks and protect client assets in mid-2026, lenders must adopt a proactive, multi-layered risk management program:

- Implement Specialized Pre-Closing Due Diligence: Require independent Plan and Specification Reviews to verify that budgets realistically reflect current metal and lumber tariff pressures.

- Mandate PFAS Screenings: Instruct environmental professionals to bypass standard Phase I limitations and perform comprehensive PFAS evaluations on all commercial assets.

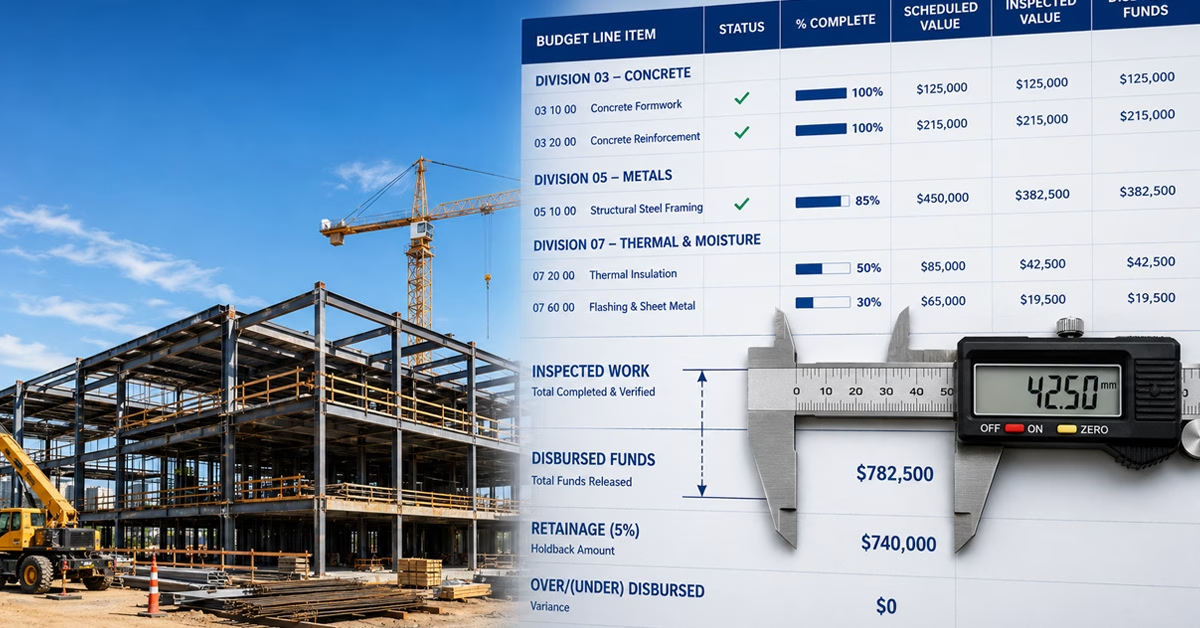

- Execute Absolute Draw Discipline: Never disburse funds based on paper invoices alone. Enforce a strict funds control program backed by geo-verified, physical inspections to ensure that work is actually completed on-site before capital leaves the bank.

- Vet the Behind-the-Scenes Operators: Perform background and credit checks on all entity members, wholesalers, and general contractors—not just the public-facing borrower.

By moving away from manual, reactive processes and partnering with experienced construction risk management experts, lenders can safely capture high-yield opportunities while ensuring their investments remain fully protected from day one to project closeout.